This report includes a dedicated chapter covering supply chain exposure, export controls, sanctions risk, and regulatory shifts affecting Automotive Suspension Market.

Market Overview

Overview

The Automotive Suspension Market is evolving from a conventional ride-comfort subsystem into a strategically critical vehicle dynamics architecture that directly influences stability, energy efficiency, passenger comfort, and intelligent vehicle control. Suspension systems connect vehicle bodies to wheel assemblies through components such as shock absorbers, springs, control arms, linkages, and dampers that regulate wheel movement, absorb road impact, and maintain tire-road contact under varying driving conditions.

As modern vehicles become heavier, more electrified, software-integrated, and performance-sensitive, suspension systems are increasingly expected to deliver more than mechanical shock absorption. They now play a central role in chassis stabilization, vehicle motion control, braking balance, steering precision, aerodynamic optimization, and sensor stability for advanced driver assistance systems.

The market is witnessing a structural transition toward electronically controlled and adaptive suspension technologies capable of dynamically responding to terrain conditions, driving behavior, vehicle load distribution, and real-time vehicle control inputs. This shift is transforming suspension systems into intelligent vehicle dynamics platforms integrated with broader automotive electronics and software ecosystems.

Role in Vehicle Ecosystem

Automotive suspension systems manage vehicle stability, ride comfort, and load distribution by controlling wheel movement and road interaction. They play a central role in maintaining handling performance and structural balance.

- Maintain vehicle stability across varying road conditions.

- Control load transfer and ride comfort dynamics.

- Support braking, steering, and handling performance.

- Integrate with vehicle chassis and control systems.

- Operate as core components within ride and stability architectures.

Suspension systems function as structural stability layers within the vehicle ecosystem, linking vehicle dynamics, ride control, and safety performance across modern automotive platforms.

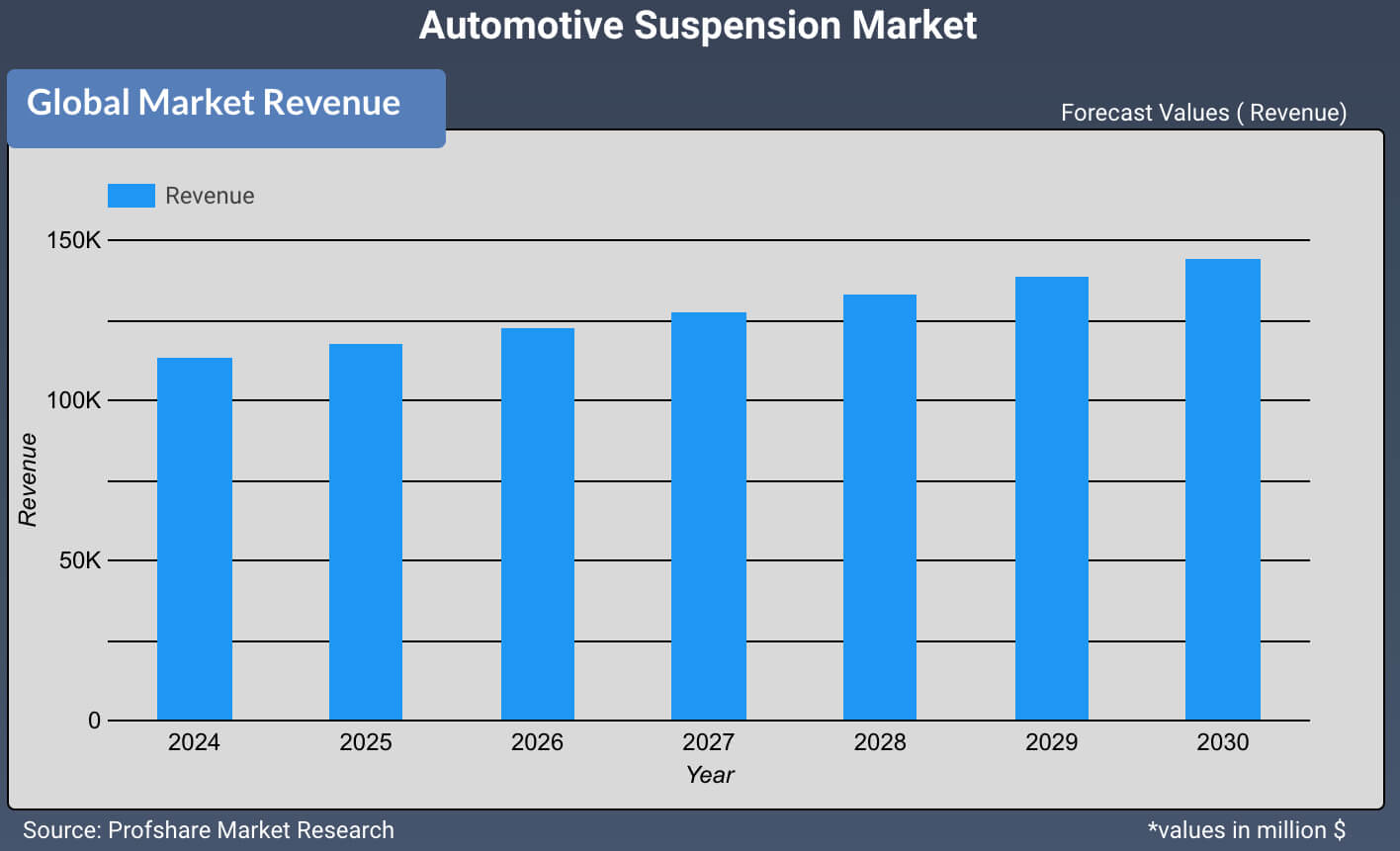

Market Forecast 2026–2032

⬇ Download Chart

Market Drivers

The Automotive Suspension Market is primarily driven by the increasing complexity of modern vehicle architectures and rising demand for superior ride stability, handling precision, and occupant comfort across passenger and commercial transportation platforms. As vehicles integrate larger battery packs, advanced electronics, and autonomous driving features, suspension systems are becoming critical for maintaining structural balance, dynamic control, and driving consistency.

The rapid expansion of electric vehicles is significantly accelerating suspension innovation. EV platforms introduce unique engineering challenges related to battery weight concentration, altered center-of-gravity distribution, regenerative braking behavior, and platform rigidity requirements. Automakers are increasingly adopting advanced suspension systems capable of supporting heavier vehicle structures while preserving ride comfort, handling responsiveness, and energy efficiency.

Growth in premium vehicles, SUVs, crossover platforms, and high-performance mobility segments is further increasing demand for electronically controlled suspension technologies that enhance cornering stability, vibration isolation, and adaptive ride characteristics. Consumers increasingly associate ride quality and cabin refinement with overall vehicle value, making suspension performance a key differentiator in automotive product positioning.

Commercial transportation expansion is also contributing to market growth, particularly in heavy-duty trucks, logistics fleets, and long-distance passenger transport. Fleet operators increasingly require suspension systems that improve durability, load management, fuel efficiency, and driver comfort while reducing vehicle wear under intensive operating conditions.

Automotive manufacturers are simultaneously focusing on lightweight suspension materials, modular chassis integration, and scalable suspension architectures to optimize vehicle efficiency, reduce platform complexity, and improve manufacturing flexibility.

Emerging Trends

One of the most significant trends shaping the Automotive Suspension Market is the transition from passive mechanical suspension systems toward intelligent, software-integrated vehicle dynamics control platforms. Modern suspension technologies increasingly interact with electronic control units, braking systems, steering systems, and vehicle motion sensors to deliver predictive and adaptive ride management.

Electronically controlled suspension and adaptive damping systems are gaining rapid adoption due to their ability to continuously adjust damping force and ride characteristics based on road conditions, vehicle speed, cornering behavior, and load distribution. These systems improve vehicle stability, passenger comfort, and handling precision while enabling real-time optimization of driving dynamics.

Air suspension systems are also witnessing accelerated deployment across premium passenger vehicles, commercial fleets, and electric mobility platforms. These technologies enable automatic vehicle height adjustment, improved load balancing, aerodynamic optimization, and enhanced ride isolation, making them increasingly valuable for EV efficiency management and commercial transportation applications.

The emergence of software-defined vehicles is further reshaping suspension architecture. Suspension systems are increasingly integrated into centralized vehicle control platforms that support drive mode customization, predictive terrain sensing, automated ride calibration, and over-the-air software updates.

Another major trend involves the adoption of lightweight materials such as aluminum alloys, composite structures, and advanced high-strength steel within suspension assemblies. Automakers are pursuing lightweight suspension configurations to reduce unsprung mass, improve vehicle efficiency, extend EV driving range, and enhance dynamic responsiveness without compromising structural durability.

Segment Insights

By suspension type, the Automotive Suspension Market includes independent suspension, dependent suspension, and semi-independent suspension systems. Independent suspension systems account for a significant share of passenger vehicle adoption due to superior ride comfort, improved wheel articulation, and enhanced handling precision.

Dependent suspension systems remain widely utilized across commercial transportation platforms because of their durability, simplicity, and high load-bearing capability. Heavy commercial vehicles, buses, and industrial transport fleets continue to rely on dependent suspension configurations for operational reliability under demanding load conditions.

Semi-independent suspension systems balance cost efficiency, packaging simplicity, and acceptable ride performance, making them common in compact and mid-range vehicle platforms.

By component, the market includes shock absorbers, springs, control arms, linkages, stabilizer bars, and air suspension modules. Shock absorbers and dampers play a crucial role in controlling oscillation and maintaining tire-road contact stability, while springs support vehicle weight distribution and ride balance.

Air suspension modules and electronically controlled dampers are emerging as high-value growth segments due to increasing integration within intelligent vehicle control systems and premium vehicle architectures.

By vehicle type, the market is segmented into passenger vehicles, commercial vehicles, and electric vehicles. SUVs and crossover vehicles are particularly driving demand for advanced suspension systems because of their higher center of gravity and heavier vehicle structures.

Commercial vehicles require heavy-duty suspension systems capable of supporting substantial payloads while minimizing structural fatigue and improving operational durability. Electric vehicles represent one of the fastest-growing segments, requiring specialized suspension engineering capable of managing battery mass distribution, increased vehicle weight, and instant torque delivery characteristics.

Regional Insights

Asia Pacific dominates the Automotive Suspension Market due to its strong automotive manufacturing ecosystem, expanding vehicle production capacity, and rising commercial transportation demand across China, Japan, South Korea, and India. The region benefits from large-scale automotive supply chains, increasing EV production, and growing demand for both passenger and heavy commercial vehicles.

China remains a particularly important growth center due to aggressive electric vehicle expansion and increasing investments in intelligent automotive technologies. Suspension manufacturers operating in the region are actively developing scalable and cost-efficient suspension systems optimized for high-volume EV platforms and commercial mobility applications.

North America is witnessing steady market growth driven by rising demand for SUVs, pickup trucks, electric vehicles, and advanced ride-control technologies. The region also benefits from strong consumer preference for premium vehicle features, including adaptive suspension systems and electronically controlled ride platforms.

Europe maintains a significant market share due to its advanced automotive engineering capabilities, strong premium vehicle manufacturing base, and accelerated adoption of intelligent chassis technologies. European automakers are increasingly investing in integrated vehicle dynamics systems that combine suspension, steering, braking, and stability control into unified software-managed architectures.

Competitive Landscape

The Automotive Suspension Market is highly competitive and increasingly shaped by the transition toward intelligent chassis systems, electrified mobility platforms, and software-defined vehicle architectures. Competitive differentiation is no longer limited to mechanical durability or ride comfort alone; manufacturers are increasingly competing on electronic integration capability, predictive control performance, lightweight engineering, and platform scalability.

Leading suspension manufacturers are investing heavily in adaptive damping systems, electronically controlled suspension modules, air suspension technologies, and integrated vehicle dynamics platforms capable of supporting next-generation electric and autonomous vehicles.

Strategic collaboration between automotive OEMs and suspension suppliers is intensifying to accelerate development of modular suspension architectures compatible with multi-platform vehicle production. Manufacturers are also pursuing scalable suspension solutions that can be standardized across passenger vehicles, SUVs, electric vehicles, and commercial transportation platforms to improve manufacturing efficiency and reduce platform development costs.

The market is additionally experiencing pressure toward lightweight component integration, supply chain localization, and cost optimization as automakers seek to balance performance enhancement with margin protection in an increasingly competitive automotive environment.

Key players operating in the market include ZF Friedrichshafen, Continental AG, KYB Corporation, Tenneco, Hitachi Astemo, Magneti Marelli, and Mando Corporation. These companies are actively developing next-generation suspension systems aligned with electrification, intelligent mobility, and software-integrated vehicle control trends.

Strategic Outlook

The Automotive Suspension Market is entering a phase of structural transformation as vehicle manufacturers increasingly prioritize intelligent ride control, chassis software integration, electrification compatibility, and platform efficiency optimization. Suspension systems are gradually evolving into active vehicle dynamics management platforms that influence not only ride comfort and handling performance, but also energy efficiency, autonomous driving stability, occupant experience, and overall vehicle intelligence.

Future market leadership will likely depend on the ability of suspension manufacturers to integrate mechanical engineering expertise with software-defined control capability, lightweight material innovation, and scalable EV-compatible architectures. As the automotive industry transitions toward connected, electrified, and autonomous mobility ecosystems, suspension technologies are expected to become increasingly central to next-generation vehicle performance differentiation and platform competitiveness.

Automotive Components Landscape

Report Coverage

| Parameter | Details |

|---|---|

| Base Year | 2026 |

| Historical Data | 2020 – 2025 |

| Forecast Period | 2026 – 2032 |

| Base Year Value | USD 109.06 Billion |

| Forecast Value | USD 144.49 Billion |

| CAGR | 4.1% |

| Regional Scope | North America · Europe · Asia-Pacific · Latin America · MEA · RoW |

Frequently Asked Questions

Automotive Suspension Market was valued at USD 109.06 Billion in 2026 and is estimated to reach USD 144.49 Billion by 2032.

Automotive Suspension Market is projected to grow at a CAGR of 4.1% during 2026–2032, driven by rising demand across industrial and specialty applications.

Automotive Suspension Market is dominated by the Passenger Vehicle segment and the Asia-Pacific region holds the highest market share in 2025.

Some of the top key players in the Automotive Suspension Market are ZF Friedrichshafen, Tenneco, KYB, Showa, Bilstein, Mando, Hitachi Astemo, Continental.

Primary driving factors for the growth of the Automotive Suspension Market include Growing demand of the automobile with better comfort features in the developing countries along with technological advancements.

Yes. The report includes a dedicated section on geopolitical risk factors and their impact on supply chains, pricing, and regional demand dynamics.